Rates

Inflation Expectations Firm Up, Driving Up Short Rates While Long Rates Fall

The Eurozone has long had persistently low inflation despite considerable QE programs, but that's changing: with inflation expectations rising, it will be important to hear what the ECB thinks tomorrow

Published ET

US TIPS 5Y and 10Y Breakeven Inflation | Source: Refinitiv

QUICK US SUMMARY

- 3-Month USD LIBOR unchanged at 0.1158%

- The treasury yield curve flattened, with the 1s10s spread tightening -4.6 bp, now at 127.0 bp (YTD change: +46.5bp)

- 1Y: 0.0660% (up 0.5 bp)

- 2Y: 0.2182% (down 0.4 bp)

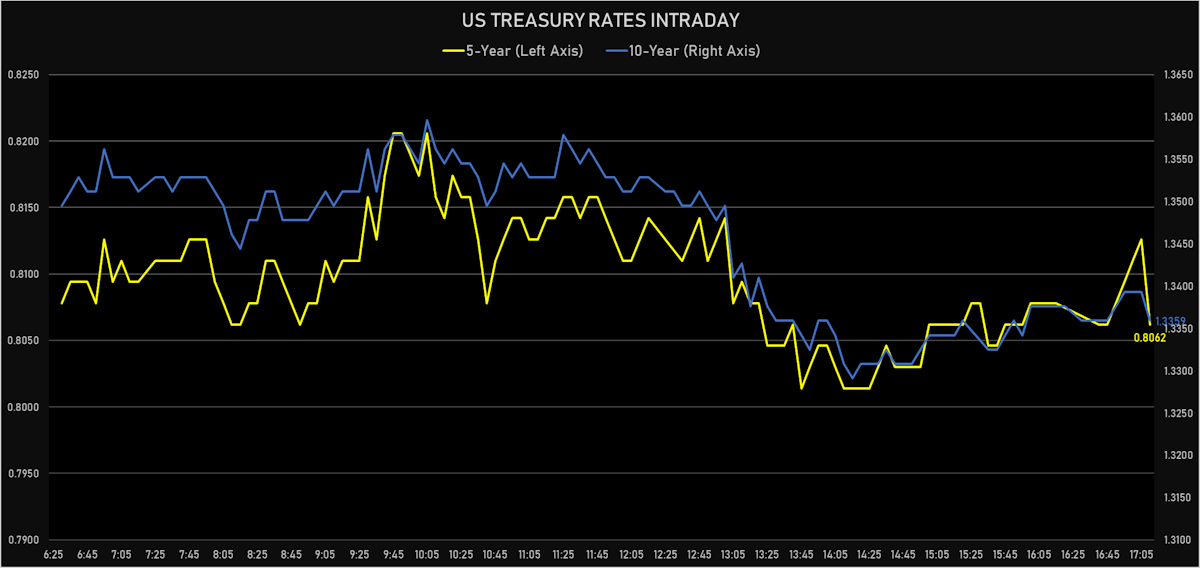

- 5Y: 0.8062% (down 1.8 bp)

- 7Y: 1.1110% (down 3.0 bp)

- 10Y: 1.3359% (down 4.1 bp)

- 30Y: 1.9550% (down 3.8 bp)

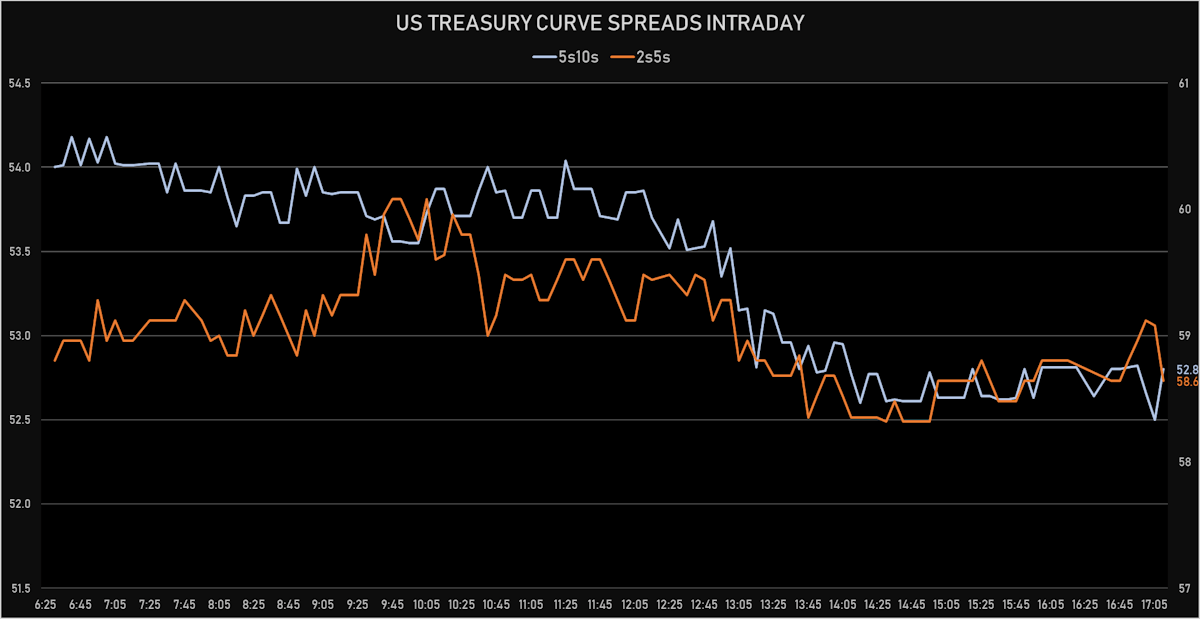

- US treasury curve spreads: 2s5s at 58.8bp (down -1.4bp), 5s10s at 53.0bp (down -2.3bp), 10s30s at 61.9bp (up 0.3bp today)

- Treasuries butterfly spreads: 2s5s10s at -6.2bp (down -0.7bp), 5s10s30s at 8.7bp (up 2.9bp)

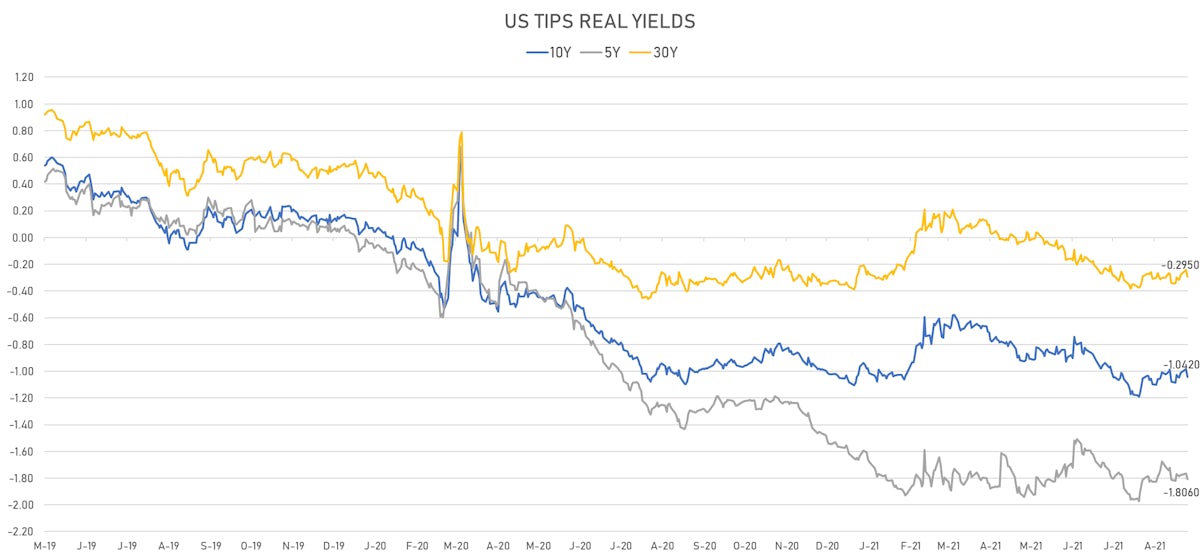

- US 5-Year TIPS Real Yield: -4.2 bp at -1.8060%; 10-Year TIPS Real Yield: -5.6 bp at -1.0420%; 30-Year TIPS Real Yield: -5.3 bp at -0.2950%

$38BN 10-YEAR TREASURY NOTE AUCTION

- Strong overall results, with good demand and impressive non-dealer bidding of 87.7% (vs. a 78.4% average)

- High yield at 1.3380%, a 1.4 bp stop-through vs. the 1.3520% at the bid deadline (-0.2 bp vs prior auction in August)

- Bid cover at 2.59x (vs 2.65x prior and 2.42x average)

- Indirect bidders at 71.1% (vs. 77.2% prior and 62.2% average)

- Direct bidders at 16.6% (vs. 13.1% prior and 16.2% average)

- Dealers at 12.3% (vs. 9.6% prior and 21.6% average)

US MACRO RELEASES

- Chain Store Sales, Johnson Redbook Index, yoy% index, Change Y/Y for W 04 Sep (Redbook Research) at 16.50 % (vs 18.60 % prior)

- Consumer credit, total, Absolute change for Jul 2021 (FED, U.S.) at 17.00 Bln USD (vs 37.69 Bln USD prior), below consensus estimate of 25.00 Bln USD

- JOLTS Job Openings for Jul 2021 (BLS, U.S Dep. Of Lab) at 10.93 Mln (vs 10.07 Mln prior), above consensus estimate of 10.00 Mln

- MBA Mortgage Applications Survey composite index, weekly percentage change, Change P/P for W 03 Sep (MBA, USA) at -1.90 % (vs -2.40 % prior)

- Mortgage applications, market composite index for W 03 Sep (MBA, USA) at 705.60 (vs 719.40 prior)

- Mortgage applications, market composite index, purchase for W 03 Sep (MBA, USA) at 258.40 (vs 259.00 prior)

- Mortgage applications, market composite index, refinancing for W 03 Sep (MBA, USA) at 3,292.10 (vs 3,385.80 prior)

- Mortgage Lending Rates, FRM 30-Year Contract Rate (MBA Sourced) for W 03 Sep (MBA, USA) at 3.03 % (vs 3.03 % prior)

- Refinitiv / Ipsos Primary Consumer Sentiment Index (CSI) for Sep 2021 (Refinitiv/Ipsos) at 59.44 (vs 57.07 prior)

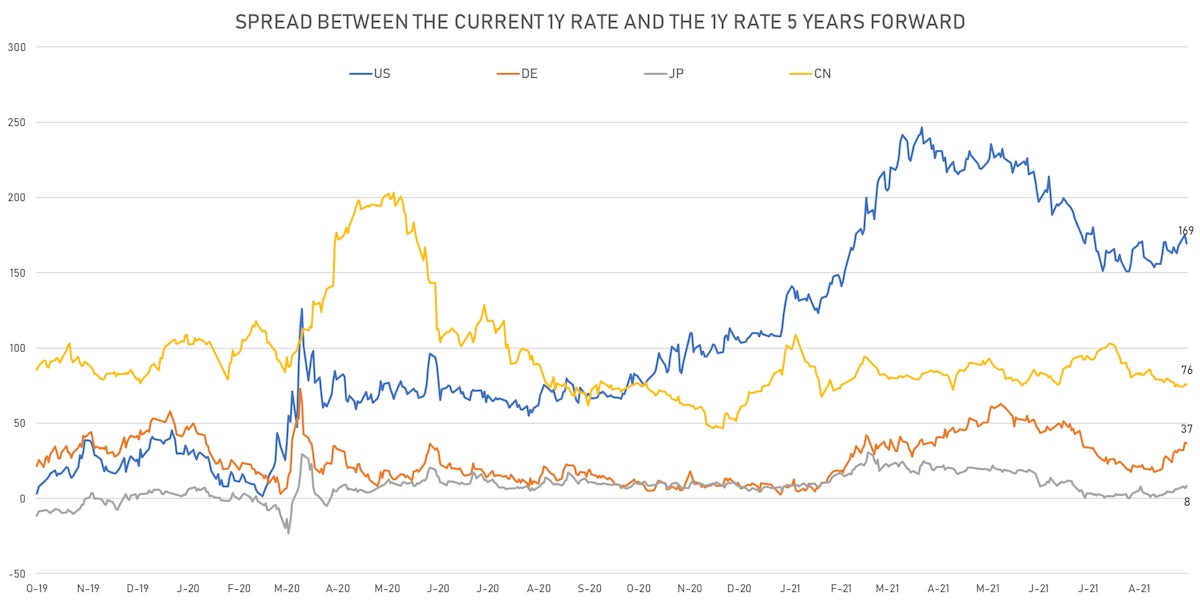

US FORWARD RATES

- US Treasury 1-year zero-coupon rate 5 years forward down 5.9 bp, now at 1.7748%

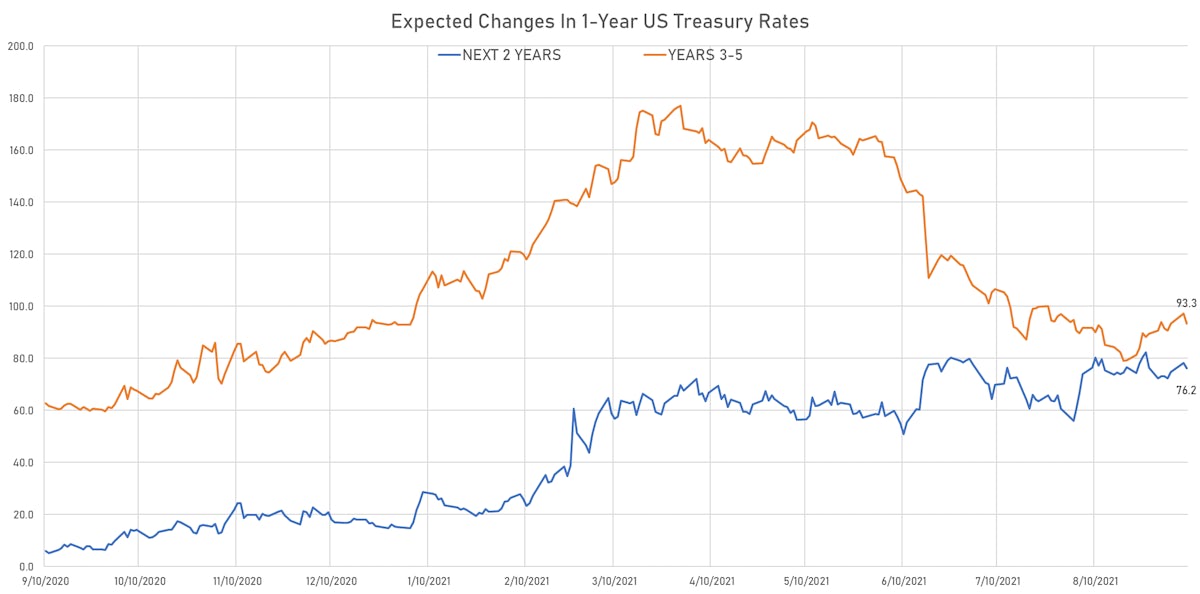

- 1-Year Treasury rates are now expected to increase by 169.4 bp over the next 5 years

- 3-month Eurodollar futures expected hike of 15.5 bp by the end of 2022 (meaning the market prices 62.0% chance of a 25bp hike by end of 2022)

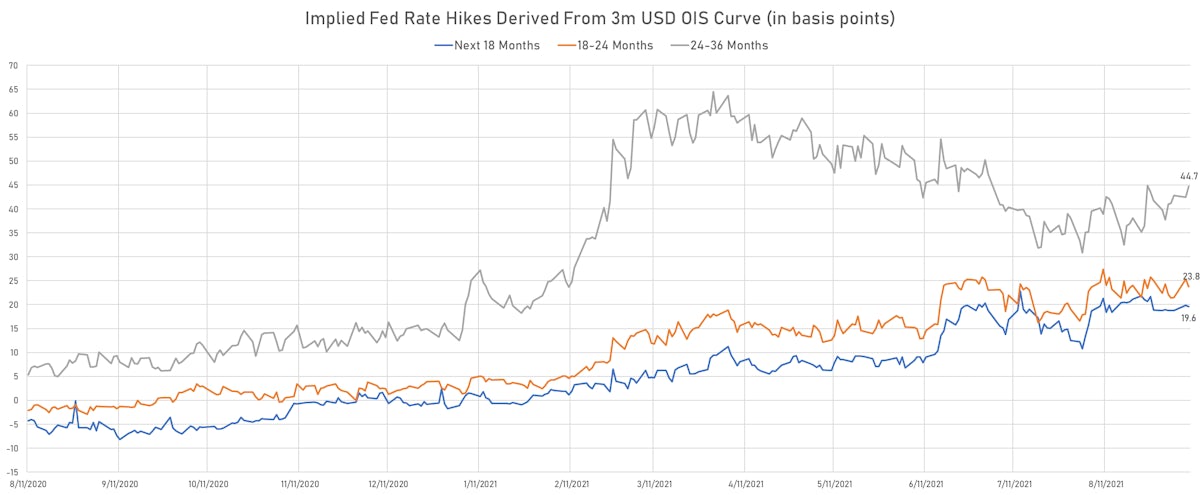

- The 3-month USD OIS forward curve prices in 19.6 bp of rate hikes over the next 18 months (equivalent to 0.78 rate hike) and 88.1 bp over the next 3 years (equivalent to 3.52 rate hikes)

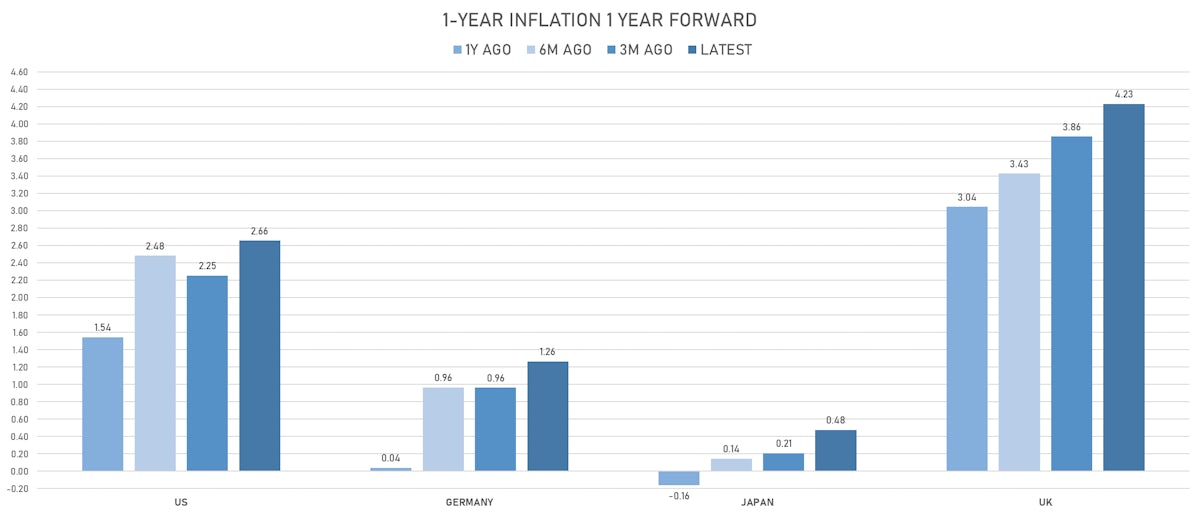

US INFLATION & REAL RATES

- TIPS 1Y breakeven inflation at 3.08% (up 4.7bp); 2Y at 2.87% (up 4.2bp); 5Y at 2.67% (up 2.3bp); 10Y at 2.36% (up 1.5bp); 30Y at 2.26% (up 1.6bp)

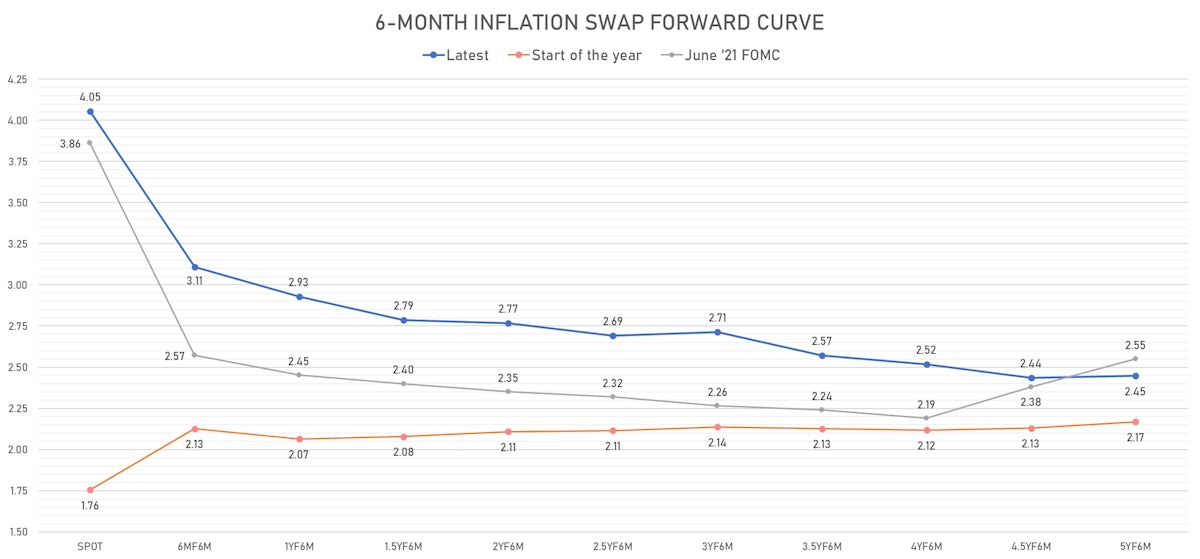

- 6-month spot US CPI swap down -1.0 bp to 4.055%, with a flattening of the forward curve

- US Real Rates: 5Y at -1.8060%, -4.2 bp today; 10Y at -1.0420%, -5.6 bp today; 30Y at -0.2950%, -5.3 bp today

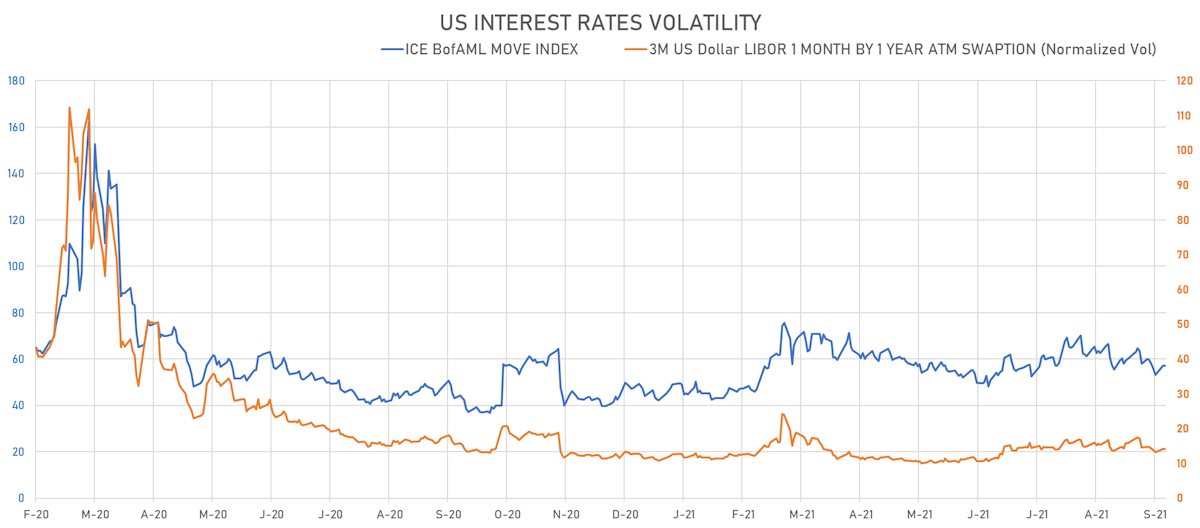

RATES VOLATILITY & LIQUIDITY

- USD swap rate implied volatility (USD 1 Month by 1 Year ATM Swaption) unchanged at 14.1%

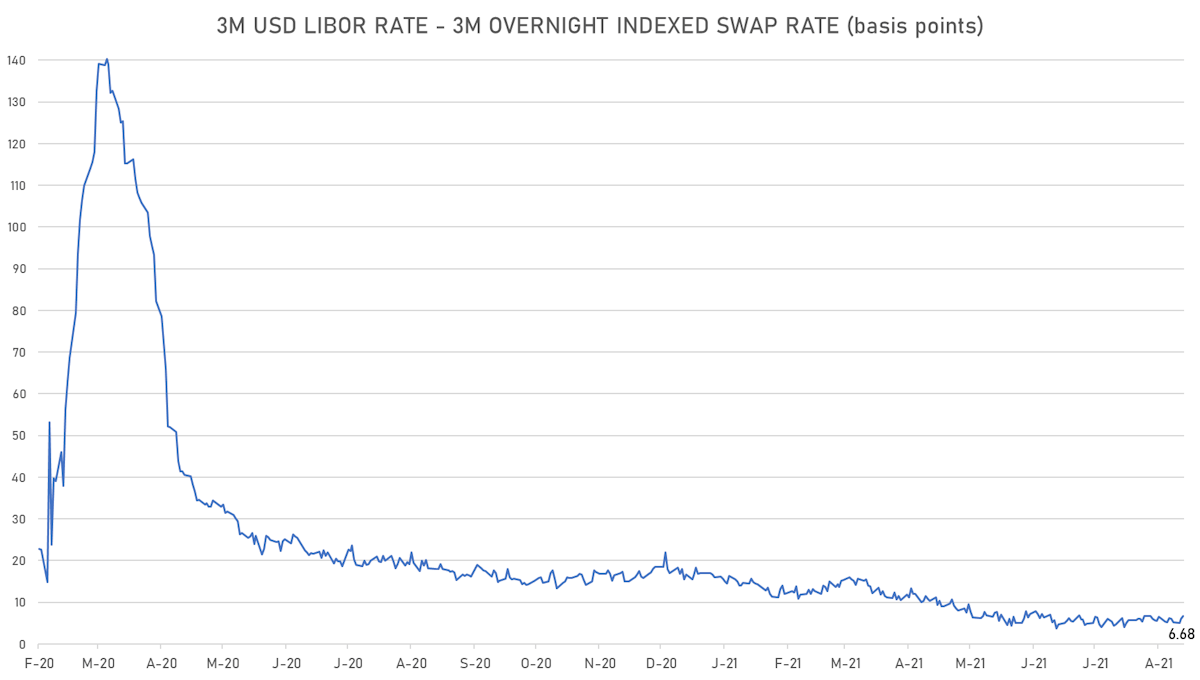

- 3-Month LIBOR-OIS spread up 0.6 bp at 6.7 bp (12-months range: 3.7-22.0 bp)

KEY INTERNATIONAL RATES

- Germany 5Y: -0.637% (down -0.5 bp); the German 1Y-10Y curve is 0.6 bp flatter at 34.1bp (YTD change: +19.6 bp)

- Japan 5Y: -0.087% (unchanged); the Japanese 1Y-10Y curve is 0.3 bp steeper at 15.4bp (YTD change: +1.0 bp)

- China 5Y: 2.685% (up 1.5 bp); the Chinese 1Y-10Y curve is 1.6 bp steeper at 61.7bp (YTD change: +15.3 bp)

- Switzerland 5Y: -0.582% (down -3.8 bp); the Swiss 1Y-10Y curve is 1.2 bp steeper at 49.3bp (YTD change: +21.2 bp)