Rates

Front-Loaded Rise In US Rates Following The Fastest Pace In Shelter Inflation Since The 2006-2007 Housing Boom

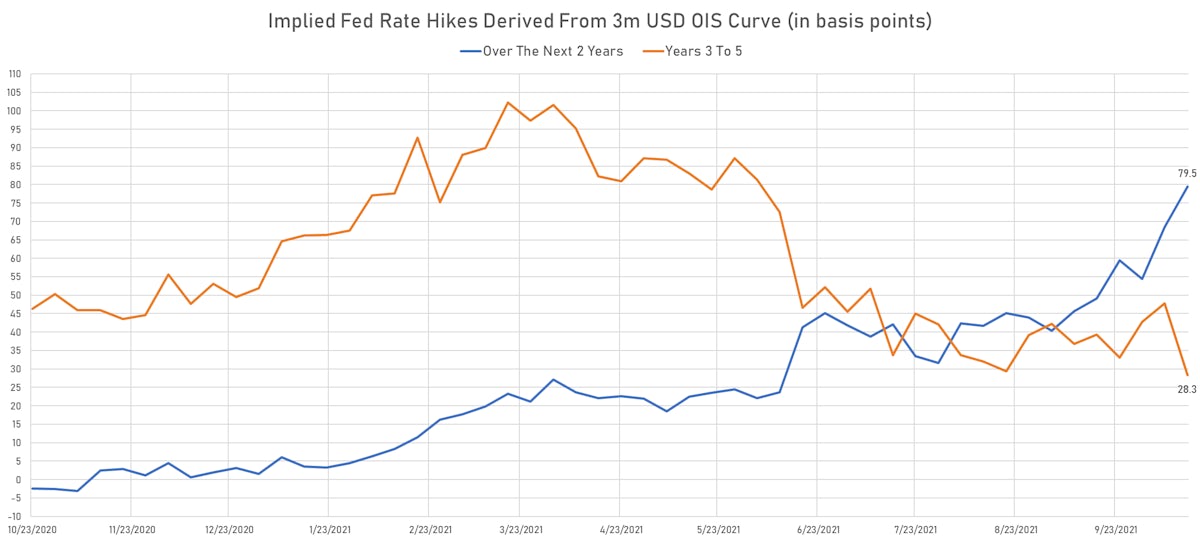

The market is currently pricing in a little over one rate hike by end of 2022 and there is room for a further rise in rates at the front end: if tapering is completed by the end of 1H22, there would be enough time for the Fed to hikes twice in 2022 (maybe in September and December) if necessary

Published ET

US TIPS Breakeven Inflation Curve | Sources: ϕpost, Refinitiv data

QUICK US SUMMARY

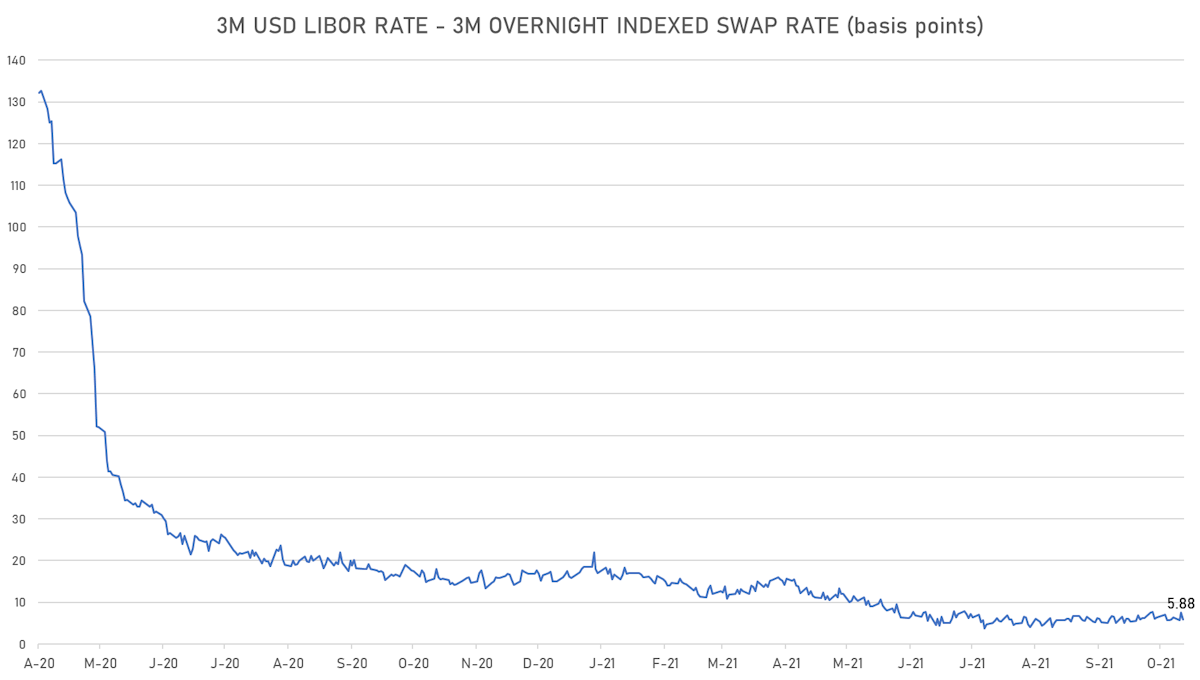

- 3-Month USD LIBOR -0.30bp today, now at 0.1238%; 3-Month SOFR OIS unchanged at 0.0520%

- The treasury yield curve flattened, with the 1s10s spread tightening -3.0 bp, now at 144.3 bp (YTD change: +63.9bp)

- 1Y: 0.0990% (unchanged)

- 2Y: 0.3600% (up 1.8 bp)

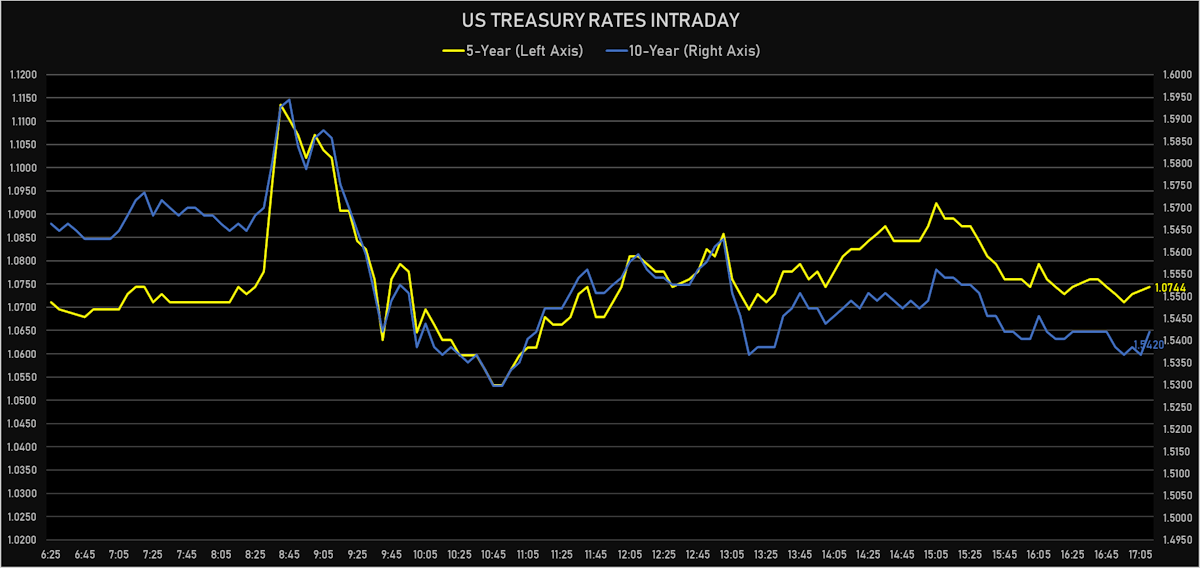

- 5Y: 1.0744% (up 0.3 bp)

- 7Y: 1.3680% (down 1.4 bp)

- 10Y: 1.5420% (down 3.0 bp)

- 30Y: 2.0336% (down 5.6 bp)

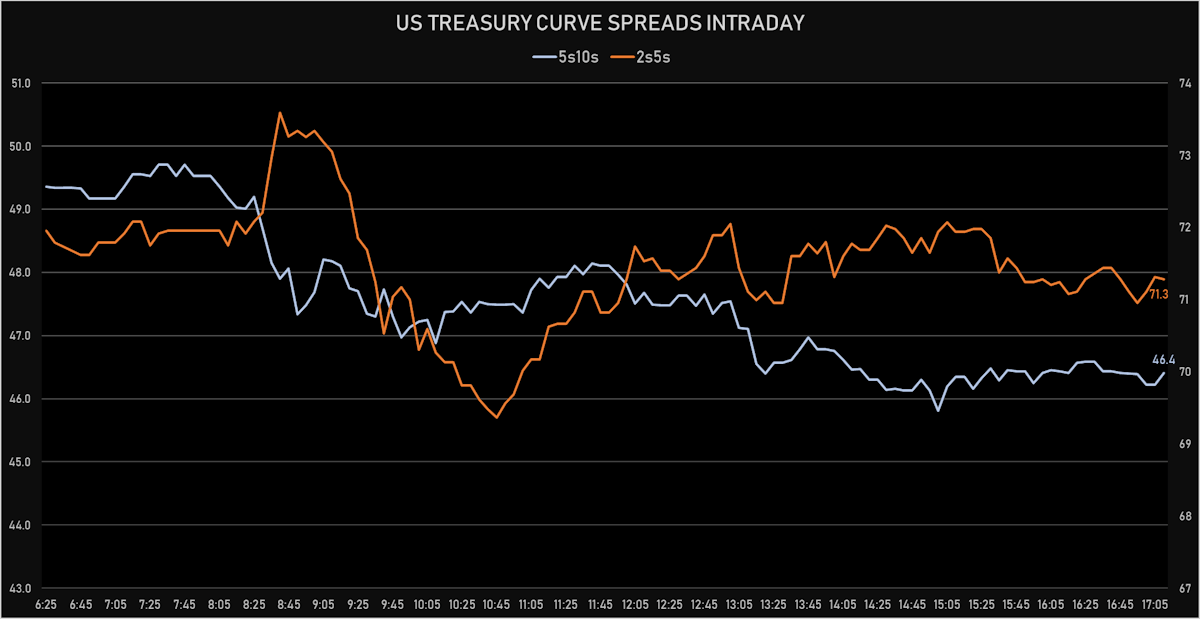

- US treasury curve spreads: 2s5s at 71.5bp (down -1.5bp), 5s10s at 46.7bp (down -3.5bp), 10s30s at 49.3bp (down -2.6bp)

- Treasuries butterfly spreads: 1s5s10s at -51.9bp (down -3.8bp), 5s10s30s at 2.2bp (up 1.5bp)

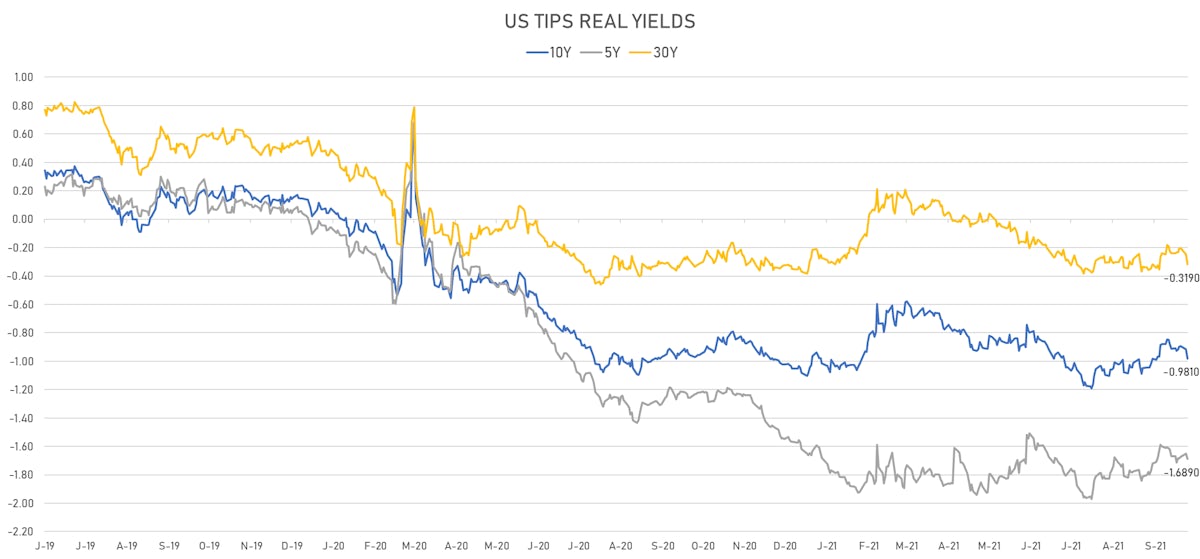

- US 5-Year TIPS Real Yield: -3.8 bp at -1.6890%; 10-Year TIPS Real Yield: -6.4 bp at -0.9810%; 30-Year TIPS Real Yield: -7.0 bp at -0.3190%

US MACRO RELEASES

- Mortgage applications, market composite index, refinancing for W 08 Oct (MBA, USA) at 3,023.00 (vs 3,037.60 prior)

- Mortgage Lending Rates, FRM 30-Year Contract Rate (MBA Sourced) for W 08 Oct (MBA, USA) at 3.18 % (vs 3.14 % prior)

- Mortgage applications, market composite index, purchase for W 08 Oct (MBA, USA) at 279.80 (vs 275.70 prior)

- MBA Mortgage Applications Survey composite index, weekly percentage change, Change P/P for W 08 Oct (MBA, USA) at 0.20 % (vs -6.90 % prior)

- Mortgage applications, market composite index for W 08 Oct (MBA, USA) at 686.10 (vs 684.50 prior)

- CPI, All items, Change P/P for Sep 2021 (BLS, U.S Dep. Of Lab) at 0.40 % (vs 0.30 % prior), above consensus estimate of 0.30 %

- CPI, All items less food and energy for Sep 2021 (BLS, U.S Dep. Of Lab) at 280.02 (vs 279.34 prior)

- Earnings, Average Weekly, Total Private, Change P/P for Sep 2021 (BLS, U.S Dep. Of Lab) at 0.80 % (vs 0.30 % prior)

- CPI - All Urban Samples: All Items, Change Y/Y for Sep 2021 (BLS, U.S Dep. Of Lab) at 5.40 % (vs 5.30 % prior), above consensus estimate of 5.30 %

- CPI, All items less food and energy, Change P/P for Sep 2021 (BLS, U.S Dep. Of Lab) at 0.20 % (vs 0.10 % prior), in line with Refinitiv consensus

- CPI, All items less food and energy, Change Y/Y, Price Index for Sep 2021 (BLS, U.S Dep. Of Lab) at 4.00 % (vs 4.00 % prior), in line with Refinitiv consensus

- CPI, All items, Price Index for Sep 2021 (BLS, U.S Dep. Of Lab) at 274.31 (vs 273.57 prior), above consensus estimate of 274.14

- CPI, FRB Cleveland Median, 1 month, Change M/M for Sep 2021 (Fed Resrv, Cleveland) at 0.50 % (vs 0.30 % prior)

- Refinitiv / Ipsos Primary Consumer Sentiment Index (CSI) for Oct 2021 (Refinitiv/Ipsos) at 57.78 (vs 59.44 prior)

US$ 24 BN 30-YEAR BOND AUCTION

- Excellent stats, with end-user demand at 87.7%, a new record high, well above the 81.1% average

- Allotted at 2.049%, 1.3bp through the 2.062% when-issued at the bid deadline

- Indirect bidders at 70.5%, third highest on record (vs 69.7% prior and 63.0% average)

- Direct bidders at 17.2% (vs 17.2% prior and 18.2% average)

- Primary dealers took in 12.3% (vs. 13.1% prior and 18.9% average)

- Bid-to-cover ratio at 2.36 (vs. 2.49 prior and 2.32 average)

US FORWARD RATES

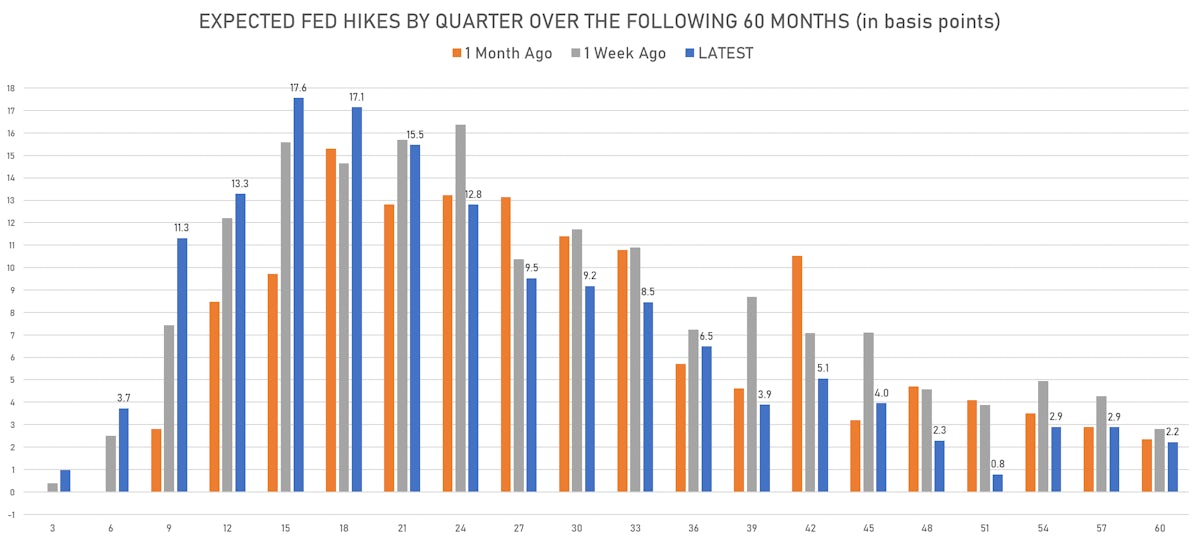

- 3-month Eurodollar future (EDU2) expected Fed hike of 28.7 bp by the end of 2022 (meaning the market prices in more than one 25bp hike by end of 2022)

- 1-month USD LIBOR FRAs imply 36.2 bp hike by the end of 2022, meaning that the FRA market expects 1.4 full hike by then

- The 3-month USD OIS forward curve prices in 119.5 bp over the next 3 years (equivalent to 4.78 rate hikes)

- The 3-month Eurodollar zero curve prices in 141.1 bp over the next 3 years (equivalent to 5.65 rate hikes)

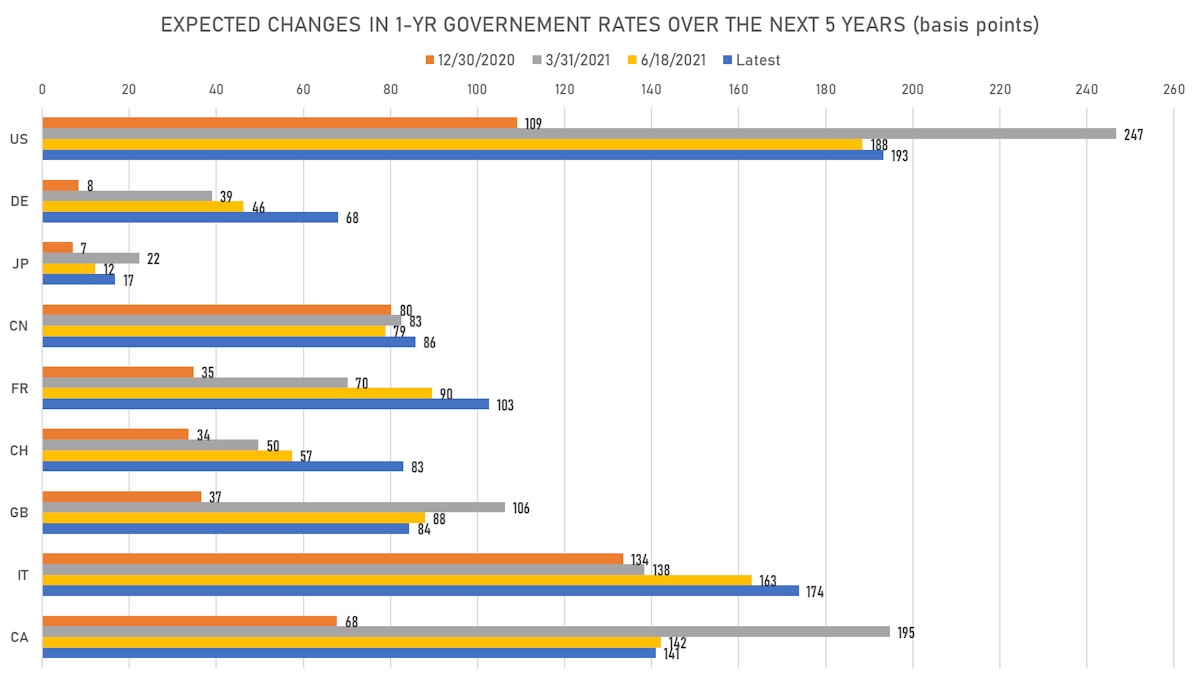

- 1-year US Treasury rate 5 years forward down 5.6 bp, now at 2.0548%, meaning that the 1-year Treasury rate is now expected to increase by 193.2 bp over the next 5 years (equivalent to 7.7 rate hikes)

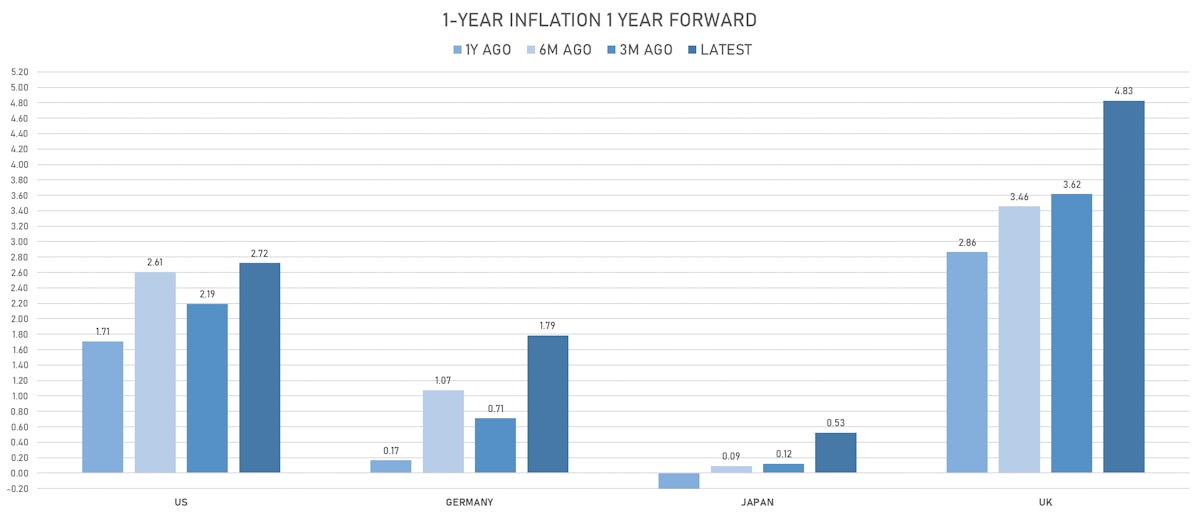

US INFLATION & REAL RATES

- TIPS 1Y breakeven inflation at 3.46% (up 11.5bp); 2Y at 3.10% (up 7.9bp); 5Y at 2.80% (up 4.2bp); 10Y at 2.50% (up 3.4bp); 30Y at 2.36% (up 1.4bp)

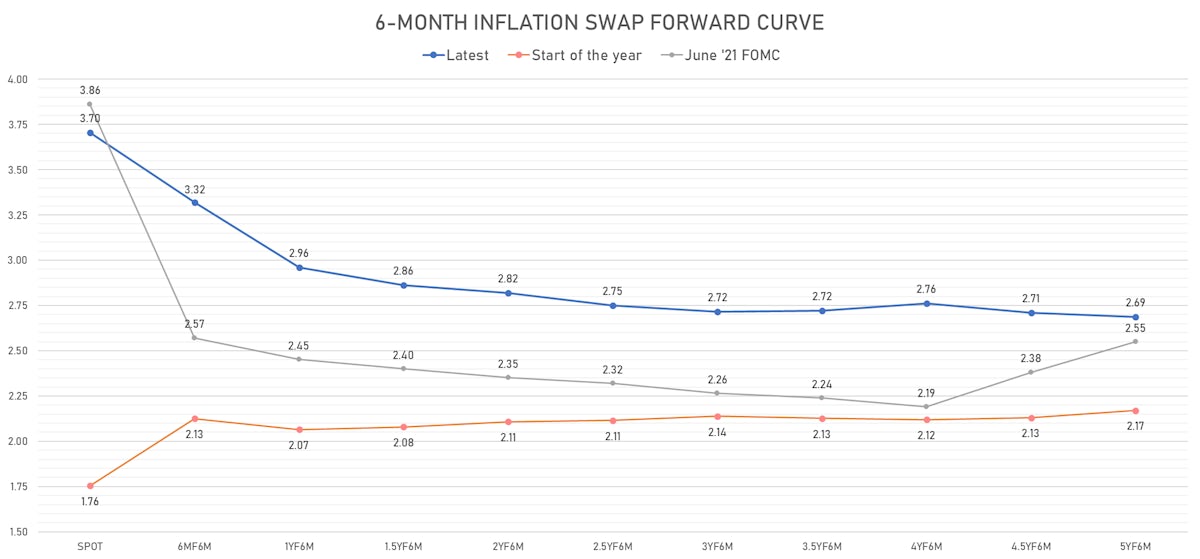

- 6-month spot US CPI swap up 9.4 bp to 3.704%, with a steepening of the forward curve (inverted)

- US Real Rates: 5Y at -1.6890%, -3.8 bp today; 10Y at -0.9810%, -6.4 bp today; 30Y at -0.3190%, -7.0 bp today

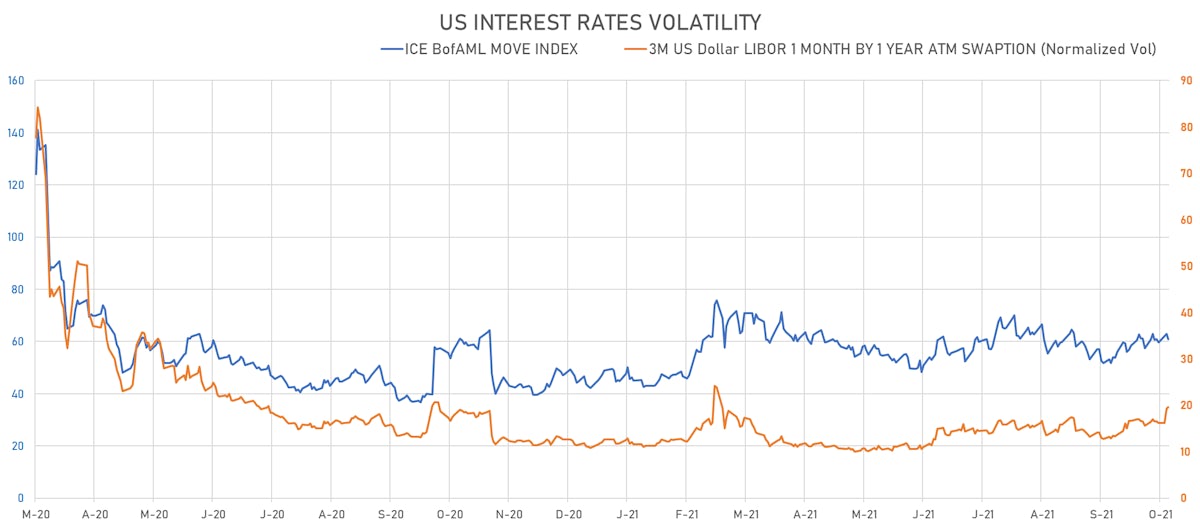

RATES VOLATILITY & LIQUIDITY

- USD swap rate implied volatility (USD 1 Month by 1 Year ATM Swaption) up 0.3% at 19.6%

- 3-Month LIBOR-OIS spread down -1.6 bp at 5.9 bp (12-months range: 3.7-22.0 bp)

KEY INTERNATIONAL RATES

- Germany 5Y: -0.479% (down -0.7 bp); the German 1Y-10Y curve is 3.2 bp flatter at 54.5bp (YTD change: +39.6 bp)

- Japan 5Y: -0.080% (unchanged 0.0 bp); the Japanese 1Y-10Y curve is 0.3 bp steeper at 21.0bp (YTD change: +6.5 bp)

- China 5Y: 2.803% (up 1.8 bp); the Chinese 1Y-10Y curve is 0.1 bp steeper at 66.7bp (YTD change: +20.3 bp)

- Switzerland 5Y: -0.443% (up 1.7 bp); the Swiss 1Y-10Y curve is 9.0 bp flatter at 66.4bp (YTD change: +32.6 bp)