Rates Volatility Likely To Remain High When Eurodollar Markets Reopen Tonight

With the latest CFTC/ IMM report showing increased net short duration positioning, and with Goldman Sachs changing drastically their Fed hikes forecast, we think rates markets may experience a continued squeeze in the coming days

Published ET

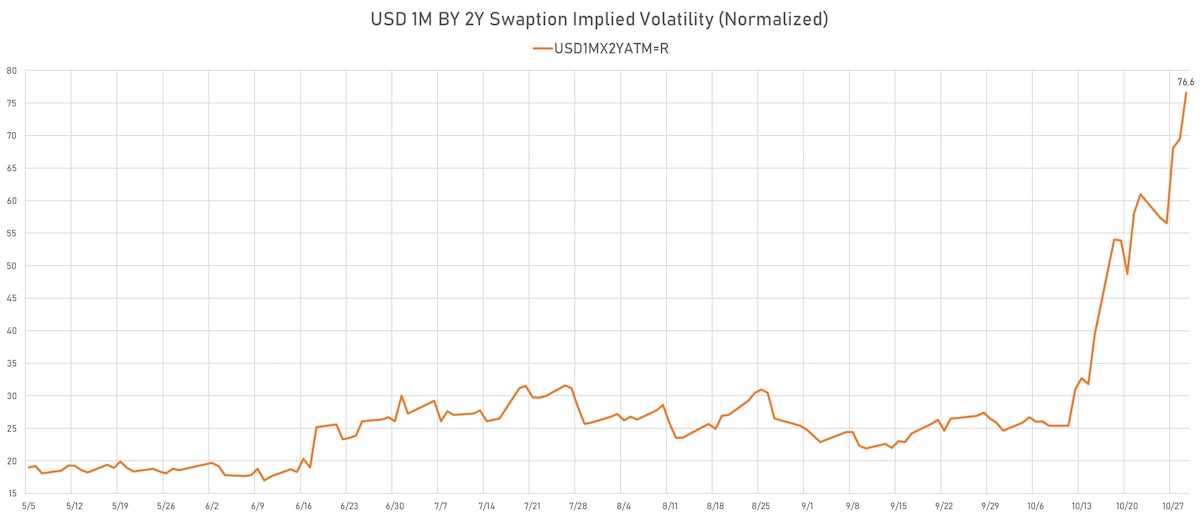

USD 1M By 2Y ATM Swaption Implied Volatility (Normalized) | Sources: ϕpost, Refinitiv data

We normally don't report on individual forecasts because they're all over the place, and generally useless for investment purposes.

But GS is changing its Fed Funds rate forecast drastically ahead of this week's FOMC:

We are pulling forward our forecast for the Fed’s first rate hike by one full year to July 2022, shortly after tapering is scheduled to conclude. We expect a second hike in November 2022 and two hikes per year after that.

We think it's worth talking about for a few reasons:

- short rates volatilities have been incredibly high this past week

- it's been a bloodbath and leveraged funds betting on a steeper curve have suffered large losses

- the CTFC / IMM report on Friday showed that specs and leveraged funds had increased (by close of play on Wednesday) the sizes of those bets

- the FOMC is 2.5 trading days away, and will finally present the long-awaited details of the Fed's policy normalization program

Now, there is nothing unusual about GS making weird or silly calls: as the premiere franchise on Wall Street, they are not known for making accurate forecasts. Instead, they often choose to make outlier calls / forecasts to pique the interest of clients and generate engagement.

The approach makes a lot of sense: when you’re a derivatives market maker, you're not going to maximize your flows by telling people that you expect the spot price in 6 months to be exactly what it is today.

This year, for example, they long held a forecast of 1.28 for the EURUSD at the end of 2021 (with a few weeks to go, we’re sitting just above 1.1560), and pushed heavily the reflation / steeper curve theme.

To be clear, we are not saying that to point out mistakes, but instead to explain that they weren’t mistakes at all: those forecasts were never meant to be accurate reflections of their thinking.

With that in mind, let's go back to the topic of the day:

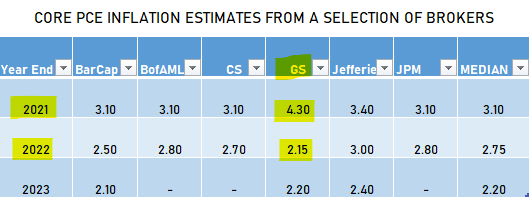

- GS says that high inflation is the justification for pulling forward their Fed Funds forecast, and yet their core inflation forecast for the end of 2022 is low compared to peers

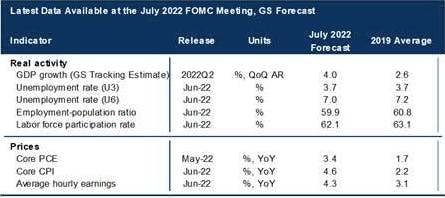

- They prepared a mock dashboard of what the Fed will have at its disposal when it makes a rate decision in July 2022

- In other words, they say inflation will be back to 2.15 by the end of 2022, but current inflation in July 2022 will be so high that they contend the Fed will be compelled to raise rates by 50bp in the meantime. Call us skeptical, but that makes no sense.

Unless we're completely wrong, this feels like a squeeze, and we have no qualms about that: the world of institutional securities is for grown-ups and there is no excuse for silly leveraged bets and poor risk management. So, if we're right, in the words of William Shakespeare: buckle up, shit’s about to get real.

We would not be surprised if by the middle of the week some sizeable funds had gone tits up. Not a forecast, but with this kind of stuff floating around, we could see rates volatility get even crazier before things calm down.

For struggling investors who hadn’t found the inner strength to commit seppuku, GS came up with a free coup de grâce in time for Halloween. And there is no doubt about the costume they've chosen this year: the grim reaper has taken the scythe out for a historic volatility harvest.