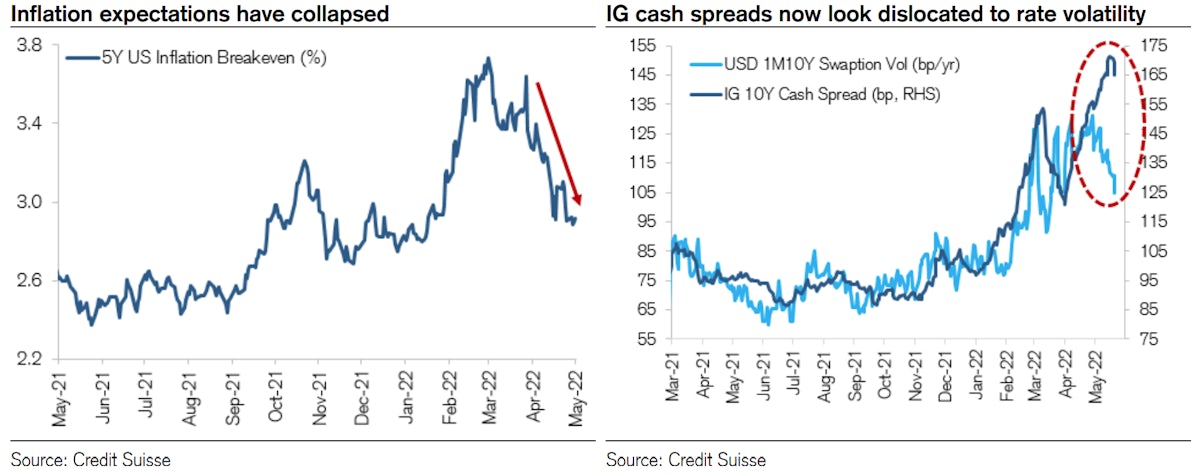

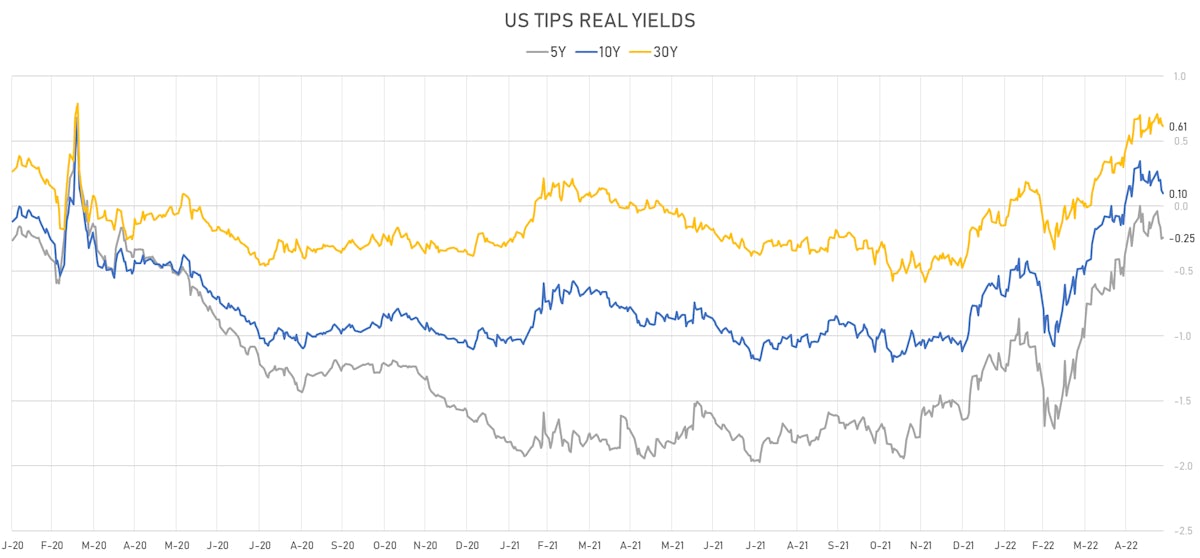

Rates

Slight Steepening In The US Treasury Curve This Week, Driven By Higher Breakevens, Higher Real Yields

The decent US macro data and reopening of Shanghai this week pushed markets to refocus their attention on central bank tightening, after spending the previous weeks pricing the risk of an imminent economic recession

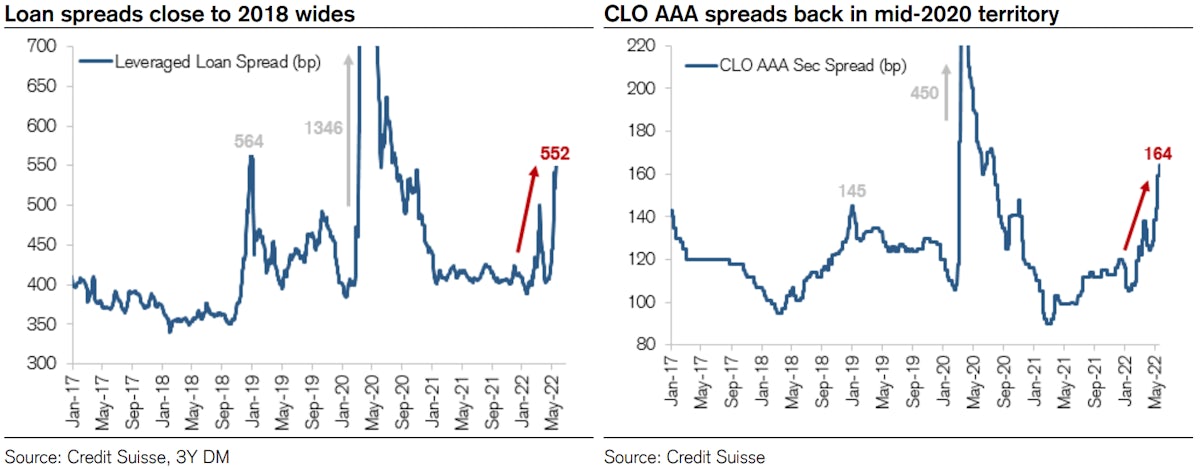

Credit

Spreads Tighter Across The Credit Complex, Although IG Cash Is Lagging In Comparison To HY Moves

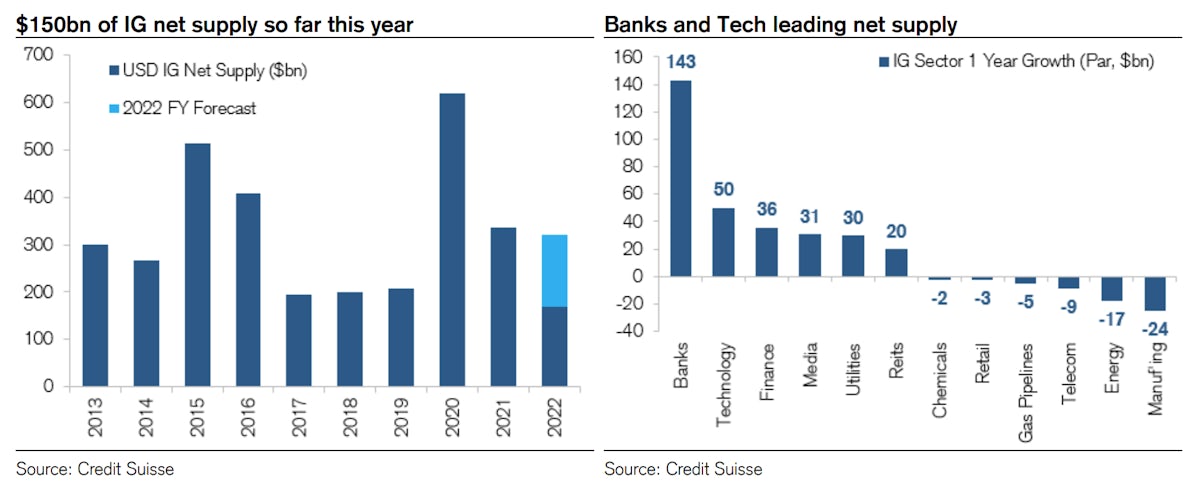

According to the IFR, it was the slowest week for US domestic IG issuance since November 2020, with just 2 tranches priced for US$700m (2022 YTD volume $652.1bn vs 2021 YTD $720.5bn ), and zero issuance in HY (2022 YTD volume $56.4bn vs 2021 YTD $248.9bn)

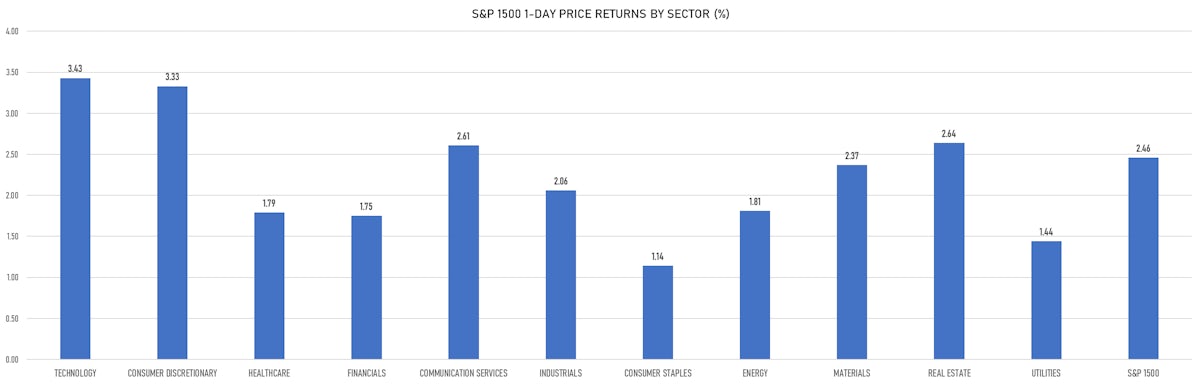

Equities

96% Up Day For S&P 500 Stock, With US Equities Ending A Positive Week Near Best Levels

Although a large number of sell-side strategists don't think equities have bottomed yet, the technical picture looks clearly tilted towards a continued rebound next week, in the context of a bear market rally for technology stocks

Rates

The US Treasury Curve Bull Steepened This Week, Driven By Lower Real Yields, While Breakevens Rose Slightly

The worry about a possible US economic recession took 9bp out of December '22 Fed funds pricing over the past week, with the September FOMC now significantly skewed towards 25bp (from 50bp a month ago); Goldman Sachs still puts the probability of a recession in the next couple of years at 35%

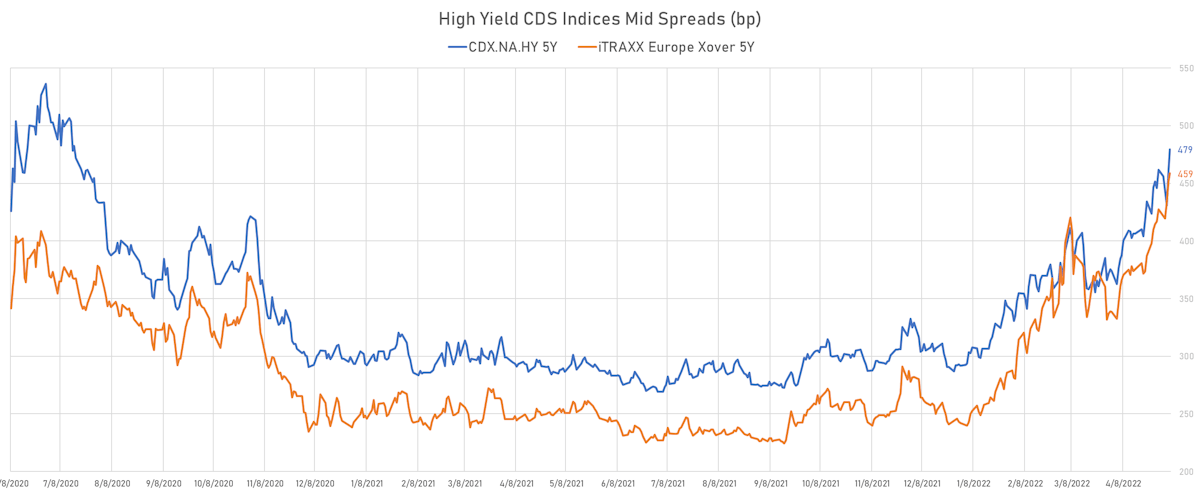

Credit

Another Volatile Week For Credit, Marked By Further Widening Of Cash OAS: +8bp In IG, +28bp In HY; CDX NA HY 5Y Implied Default At 32% (30% Recovery)

New issues in USD high yield are almost nonexistent (2022 YTD volume at just $56.4bn vs 2021 YTD $238.3bn), with Carnival the sole print this week, while the USD IG primary market was pretty active: 43 new tranches for $33.4bn (2022 YTD volume $651.4bn vs 2021 YTD $682.6bn)

Equities

Equities Continue To Slide, Though Weakness Is Now Led By Falling Economic Growth Expectations Hitting The Consumer Staples And Consumer Discretionary Sectors

Looking at Walmart's earnings miss this week, the consensus seems too high for 2023: S&P 500 earnings per share are projected to grow by 10% next year, but further gross margin expansion is unlikely, as corporate pricing power is hitting a limit (wages growing slower than inflation at the moment)

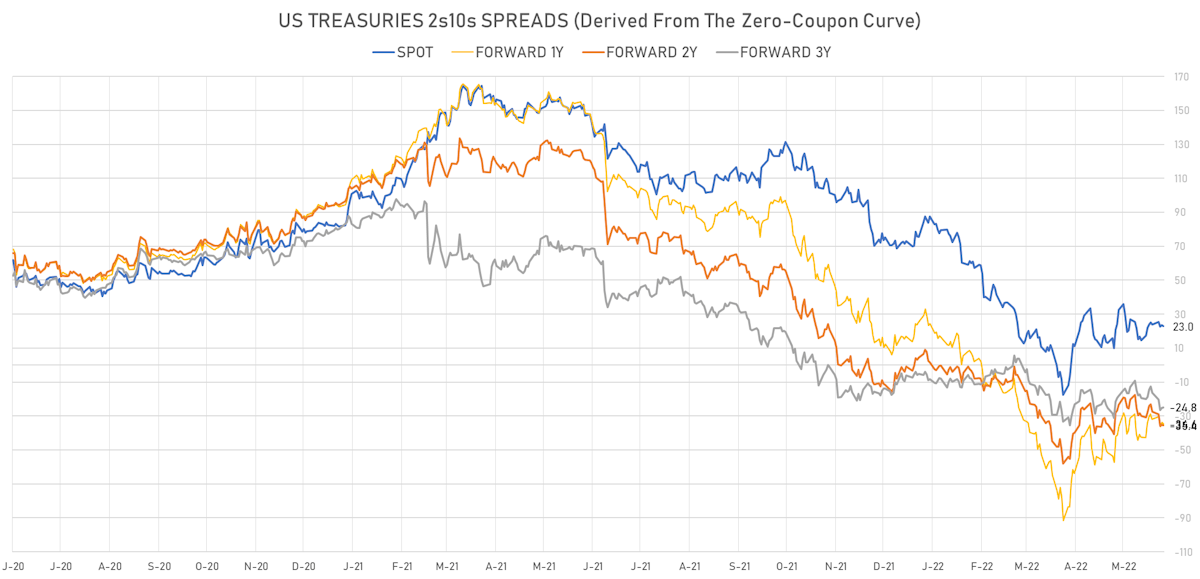

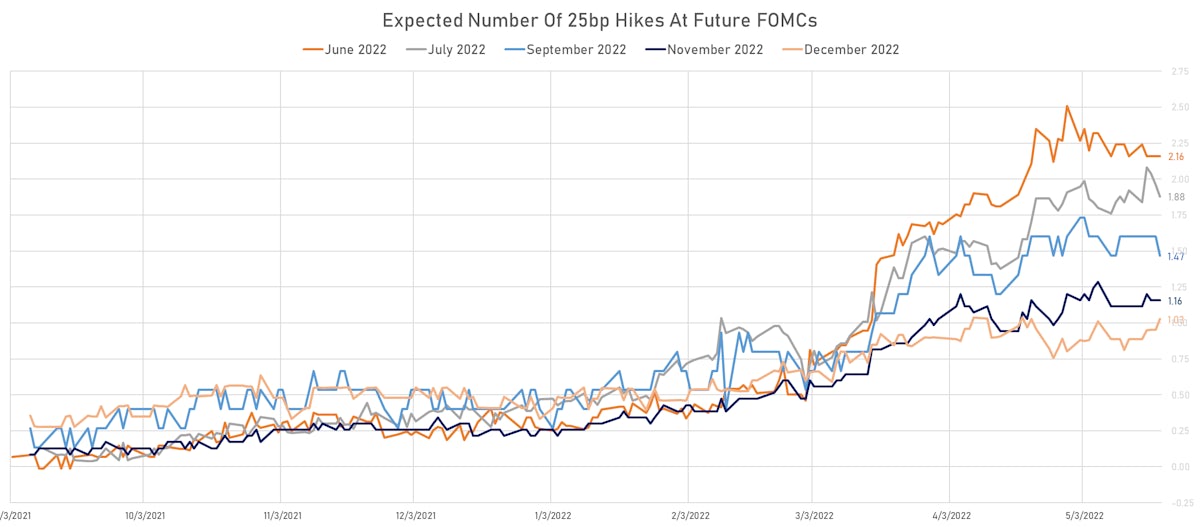

Rates

The US Curve Flattened From 2Y Out This Week, With The Front End Staying Well Anchored And 10Y Treasury Yields Coming Down 14bp

Money markets are still pricing in 50bp hikes for the next 3 FOMCs, with the most uncertainty on the September meeting, which could see the Fed decide to go for 25bp if the economy started to show signs of slowing too rapidly

Credit

Much Wider Spreads In Cash Indices This Week, With A Sizeable Compression In The CDX.NA.HY Cash Basis

Decent volumes of issuance for USD investment grade bonds this week considering the amount of volatility in risk markets: $22.1bn in 31 tranches (IFR data), with the largest offering coming from Intercontinental Exchange ($8bn in 6 tranches); only one deal priced in the HY primary market ($1.2bn)

Equities

Huge Bounce In US Equities Into The Weekend, As Over 92% Of S&P 500 Stocks End Higher on Friday

Despite the return in risk appetite today, it was a rough week for stocks, with Goldman Sachs pointing out that their prime brokerage business saw the largest 5-day reduction ever in gross leverage for fundamental long/short hedge funds

Rates

US Treasuries Bull Flattened This Week, Mostly Driven By Lower Breakevens As Fear Of Recession Beat Down Inflationary Concerns

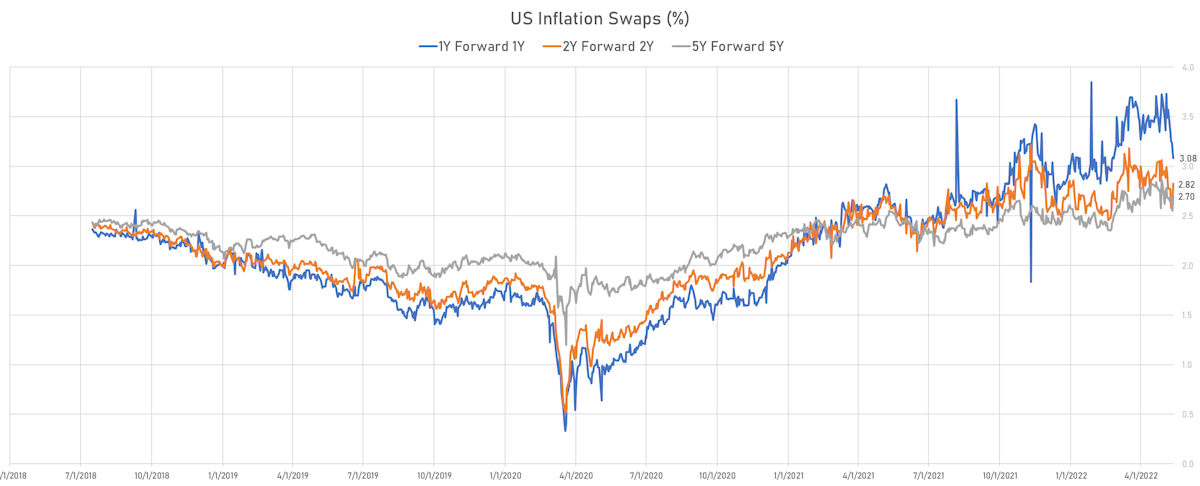

It is worth noting that short-term inflationary pressures are falling while longer-term expectations are settling higher, with an overall flattening of the inflation curve

Equities

Higher Real Yields Brought Extensive Losses To US Equities After The FOMC, Leaving Just 27% Of S&P 500 Stocks Above Their 50 DMA

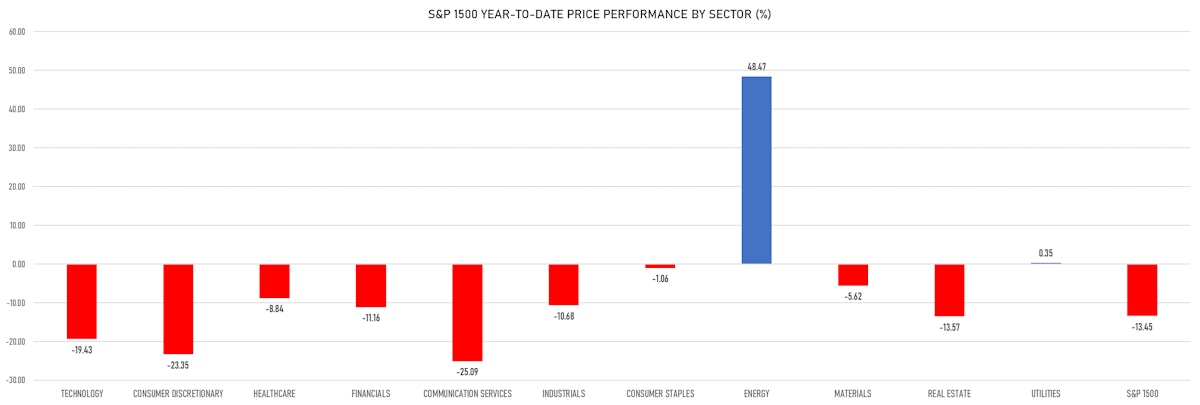

In line with other risky assets, equities continue to trade very poorly: energy is the only sector now at a 12-month high, with communication services and consumer discretionary both down close to 30% from their 12M high

Credit

Significant Spread Widening Across The Credit Complex, As Tighter Financial Conditions And Slower US Earnings Growth Weigh Heavily

Weekly volumes of USD bond issuance (IFR data): $18.2bn in 25 tranches for IG issuers (2022 YTD volume: $595.9bn vs 2021 YTD: US$608.9bn), while no deal was priced in high yield (2022 YTD volume: 85 Tranches for $54.2bn vs 2021 YTD: 314 for $210.9bn)